Ruble or foreign currency deposits: what is more profitable to keep money? In what currency is it more profitable to keep money Shares of private companies: “It’s hard to guess even for a professional here”

Rubles, euros or dollars? We all counted on a simple example.

Why is this article on the site: the question of keeping money is now more relevant than ever. But not everyone takes a pen, paper and calculator to compare different deposits.

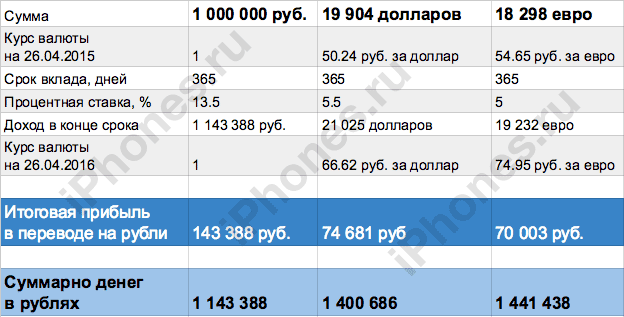

Given: hipster Arseniy, banker Veniamin and housewife Varya put money in the bank for 1 year in three different currencies.

Find: who earned more.

- 1 dollar cost 50.24 rubles,

- 1 euro - 54.65 rubles. (yes, it used to be)

Hipster Arseniy decided to open a deposit in rubles at 13.5%. This is the easiest way, thought Arseny, and decided not to take a steam bath purely.

Banker Benjamin, as a serious man, chose dollars and bought as many as 19,904 "greens", after which he took them to his bank and deposited at 5.5% per annum. Benjamin expected that the dollar would rise in price in a year, so he would be able to earn even more. We'll find out soon.

Housewife Varya dreamed of going to France in a year, so she bought 18,298 Euro and opened an account under 5%. She also hoped and believed.

Before us are three typical contributions and full adherence to the theory of the former Minister of Finance of the Russian Federation Alexei Kudrin from 2004, which reads:

A basket of currencies is the same basket, but you need to put your savings in three different baskets.

In 2016, Kudrin lectured to schoolchildren and also taught that money should be kept in three currencies.

Who of the three investors won, and who is the loser? Any of us could have been in their place.

This morning, all three, looking through the news, learned that Sberbank has sharply reduced rates on ruble deposits and practically zeroed them on deposits in foreign currency, explaining that it is time to de-dollarize the banking system, otherwise Russian depositors hold more than 50% of all deposits in dollars and euros. deposits. Well, this is understandable, because no one has canceled the theory of three baskets. The population diversifies risks in this way: if the ruble weakens, which happened during the year, then the dollars and euros will “pull out” the family budget.

Sberbank, as the locomotive of the banking sector, will soon be followed by others.

Alexander Danilov, an analyst at Fitch, believes that the dollarization of deposits is dangerous because banks have to immediately increase foreign exchange assets in order not to incur losses in the event of a devaluation. But this, in turn, leads to an increase in foreign currency loans, which creates increased risks, since the number of reliable borrowers with foreign exchange earnings is limited.

It follows from the statistics of the Central Bank that in 2015 the population bought almost $12 billion worth of cash currency - four times less than in 2014. At the same time, the population in general managed to earn about 9% of income from this.

Now that we have all the figures before our eyes, let's calculate the profit of our investors in terms of rubles.

- Hipster Arseniy put 1 million rubles, and a year later received 1 143 388 (+143 388 rubles)

- Banker Veniamin deposited 19,904 USD, and a year later he was given 21,025 (+1,121 USD) at the cash desk. Or RUB 74,681 arrived, which is almost TWO TIMES LESS than that of the hipster Arseniy.

- Least of all "lucky" housewife Varya. A year later, the girl received 19,232 euros (+934) in her hands and earned only RUB 70,003

- 1 dollar cost 66.62 rubles. (+16.38),

- 1 euro - 74.95 rubles. (+20.30)

This is not the end of the story

In total, in rubles, the following amounts were on hand:

Rubles hipster - 1,143,388 rubles.

dollars banker - 1,400,686 rubles.

Euro housewives - 1,441,438 rubles.

We asked our heroes to give all the numbers and brought everything into one table.

Conclusion

The most profitable way to store money turned out to be euros, then dollars, and at the end only rubles.

![]()

Most of the experts interviewed by the agency tend to think that the most reliable and proven way to keep savings is a bank deposit.

No matter how exchange rates change, real estate prices are all tools for professional market participants and investors, Igor Zhigunov, First Deputy Chairman of the Board of the Housing Finance Bank, told Tatar-inform news agency.

“The rate on deposits, though not high, but allows you to cover the losses from inflation. Secondly, state insurance of deposits up to 1.4 million rubles is an important element for consumers to reduce the risk of losing money. The bulk of the deposits is much less than the amount of 1 million rubles, even,” he said.

The National Bank of the Republic of Tatarstan called bank deposits an easy way to save and increase your money, which can be used by any citizen of Russia if he is 14 years old.

“Deposits can be opened not only in rubles, but also in foreign currency. In addition, it is possible to keep money on depersonalized accounts of precious metals, - told IA "Tatar-inform" in the department of the Central Bank of the Russian Federation. - It is not recommended to keep large amounts in one currency, it makes sense to keep funds proportionally in rubles, dollars and euros. So your funds will be protected from a sharp change in the exchange rate of any one currency.

Some banks provide the opportunity to open a multi-currency deposit, the bank added. Any currency specified in the contract is deposited on it. You can exchange it for another on the account itself (but they will charge a commission for the conversion). Interest on the deposit is calculated separately in each currency.

Government securities and bonds

If we are talking about savings, which in no case should be lost, then there are not many options for saving them, Igor Kokh, head of the Department of Securities, Exchange Business and Insurance of KFU, shared with Tatar-inform news agency. These are either bank deposits, which we have already mentioned, or government securities and bonds, "which also have government protection and bring a fixed income."

“In both cases, you will receive exactly as much as you should have received, regardless of any circumstances,” the doctor of economic sciences emphasized.

To purchase special government bonds, you can go to the nearest Sberbank branch, Koch advised. If we are talking about market bonds, you need the help of brokerage companies with which you will conclude an agreement and get access to operations on the Moscow Stock Exchange. There you can buy and, if necessary, sell, including government bonds.

“It is clear that for an ordinary person it can be difficult. For a person far from financial matters, the simplest and most obvious instrument is a bank deposit, although the yield on government bonds is much higher. Say, now the yield on government securities is about 8 percent per annum, on deposits - 5-6, maximum 7 percent,” Igor Kokh said.

Analyst of Finam Group Sergey Drozdov said that now there is a decrease in demand for Russian federal loan bonds, which he associated with the decision to raise VAT to 20 percent and the tightening of the monetary policy of the US Federal Reserve.

“According to our estimates, the increase in VAT will lead to a gradual acceleration of inflation from the current 2.4 percent to 3.5–3.9 percent over the current year and up to 5–7 over the next year. A possible increase in inflation has already led to the suspension by the Bank of Russia of the policy of reducing the key rate. Now the key rate is 7.25 percent, and the probability of its reduction in the second half of the year is low,” he said.

The main law of investing: profitability is proportional to risk, profitability grows - risk grows, the agency was told in the National Bank of the Republic of Tatarstan. Therefore, it is better to start with the least risky and most predictable instruments: bonds, preferred shares or investment fund units with a high credit rating.

Shares of private companies: “It’s hard to guess even for a professional here”

As for the shares of private companies, Igor Kokh, Head of the Department of Securities, Stock Exchange and Insurance of KFU, noted that one should understand how reliable this or that company is.

“If we take such companies as Gazprom or Sberbank, then their bonds give about the same yield as government bonds. Shares are a speculative instrument in principle, they either fall or rise in price, it’s hard to guess even for a professional,” Koch said.

AP Photo / Richard Drew

AP Photo / Richard Drew

The Finam Management Company was advised to pay attention to short-term corporate Eurobonds with low refinancing risks in order to hold them to maturity.

“Such securities include, for example, the issue of VEON (formerly VimpelCom Ltd.) with maturity on February 13, 2019 and the subordinated issue of Alfa-Bank with maturity on September 26, 2019. According to Eurobonds, now there is an opportunity to fix the yield to maturity at the level of 5% per annum,” Drozdov said.

As for Russian stocks, despite the state of some uncertainty in which the Russian market is located, brokers suggest that investors pay attention to ordinary shares of Sberbank, whose business remains on a growth trajectory.

“This year we expect the company to reach record profits, and since Sberbank shares are now traded at attractive multiples on the stock exchange, we believe that the decline in quotations provides an interesting opportunity to open long-term positions in these securities. This year, Sberbank's profit is projected to grow by 12 percent, to 843.8 billion rubles, according to the results of 2018, with the payment of 40 percent of profit under IFRS, the dividend on ordinary shares could be about 15 rubles, which gives an expected yield of 7 percent, and is quite high for a blue chip,” the analyst added.

In addition, in the short term, it is reasonable to pay attention to Eurobonds of Russian corporations, as well as cheaper Russian ruble bonds, Drozdov said.

“It is always better to keep money in the currency that you operate in life”

For those who are not very versed in the intricacies of the stock and debt markets, the easiest way to keep savings remainsbuying a basket of currencies, consisting of the US dollar and the euro, Sergey Drozdov told IA "Tatar-inform".

“Among the currencies of developed countries, the most successful dynamics is demonstrated by the US dollar. The Swiss franc and the Japanese yen also deserve attention - a set of traditional safe-haven currencies that usually maintain their value and even grow in troubled times,” said Vadim Iosub, senior analyst at Alpari.

The opinion of analysts was not shared by Doctor of Economic Sciences Igor Kokh.

“It is always better to keep money in the currency that you operate in life. That is, you receive income, make expenses, most likely in rubles. Accordingly, it is better to store in rubles,” the source said.

The fact is, Koch explained, that foreign currency tends to grow very quickly, but for a short time, and then remain at the same level for a long time or even decline.

“If you did not guess the moment when you need to buy a currency and bought it at a very high price, then you can stay with nothing for a very long time or even lose. In 2014, people bought dollars at 100 rubles at exchange offices. Well, actually, what to do with these dollars for 100 rubles now? Therefore, it is not necessary to try to invest in foreign currency during a period of panic and an acute crisis, because in fact this will only lead to losses, ”the expert expressed confidence.

For people willing to take risks: cryptocurrency, crowdfunding, life insurance

There are a lot of opportunities for investment and savings, you need to be aware of whether you want to save what you have or earn, Koch said.

“But if you take risks, you must understand that you can lose part of what you have invested or even all that you have invested,” the head of the department warned.

The National Bank of the Republic of Tatarstan drew attention to such a tool as crowdfunding.

“You can invest in other people's projects in order to earn. For example, with the help of crowdfunding, you can invest in startups and fast-growing companies. However, this method of saving and accumulating money is very risky,” the Bank of Russia branch noted.

In addition, there is investment life insurance. In this case, the insurance company will invest the money for you. You conclude a contract with it for 3-5 years, deposit money one or several times during this time, and at the end of the term you receive back your contributions plus the accumulated investment income.

“But remember: the funds you contributed are not insured by the state, if the insurance company goes bankrupt, you will lose your money,” the National Bank of the Republic warned.

“Frankly dubious” tool Koch called investments in cryptocurrency.

“Those who want to make quick money resort to this method, while taking a big risk. Often without even realizing what they are risking. Cryptocurrency is also a currency, only its price spikes are much higher than those of a regular currency. If you recall the same bitcoin, over the past six months it has depreciated three times. Therefore, you need to understand that anyone who deals with such tools runs the risk of losing a lot and very quickly. Only the money that you can afford to lose should be directed to such operations,” the source said.

What methods should be avoided?

The citizens of the country are now in a situation where their national currency and the domestic stock market are under pressure from external factors. More sanctions are being prepared, oil has fallen from $80 to $73 per barrel of Brent, global commodity wars are raging, now one or another currency from emerging markets is heading down: the latest relevant story is with the Turkish lira, Tatar-inform told IA senior analyst at Alpari Vadim Iosub.

“In such a situation, and with continued uncertainty about the future, it is difficult to recommend keeping all savings in the Russian ruble or Russian shares. Gold is not a worthy alternative either, which, according to Alpari, recently fell below $1,195 per troy ounce and updated its lows since January last year,” he said.

“When you want to sell it, turn it into money, it will take a lot of time, and for the sake of urgency, you will have to sell it at a significant discount,” the analyst concluded.

Put money into circulation

Another investment option for those who are willing to take risks is to invest in a business. Moreover, it can be either someone else's (the same crowdfunding, financing startups), or your own business. This option is suitable for those who do not want to work "for their uncle."

There are a lot of options for starting your own business - production, trade, franchising, Internet commerce, etc. Fortunately, now there are many programs to support small and medium-sized businesses, which, among other things, provide assistance at the very initial stage from preferential rent and taxes to assistance in obtaining loans and purchasing equipment for production.

The main thing is to remember that money should “work”, and not gather dust in a piggy bank. This is exactly the advice given by the founding father of the United States, whose face adorns the 100-dollar bill to his compatriots.

Five shillings put into circulation makes six, and if these last are again put into circulation, there will be seven shillings threepence, and so on, until one hundred pounds is made. The more money you have, the more it generates in circulation, so that profits grow faster and faster. Whoever kills a pregnant pig destroys all her offspring to the thousandth of her penis. Whoever produces one piece of five shillings kills all that it could produce: whole columns of pounds, wrote Benjamin Franklin in Advice to a Young Trader.

photo: Egor Nikitin

Discuss()

Do not rush to transfer rubles to dollars and euros on bank deposits

Roman Markelov

By the end of the year, the dollar may cost 36 rubles, and the euro will approach the mark of 50 rubles, RG experts predict.

Which does not seem like some kind of fantasy today. This week, the exchange rate of the ruble stormed from side to side, the euro, for example, came close to 46 rubles. But all this is not as scary as it seems, experts say.

There will still be fluctuations. Remember, last week on Monday and Tuesday, the ruble first partially won back its past losses, strengthening both against the dollar and against the euro. But already on Wednesday there was a rollback. And our main competing currencies managed to regain everything they lost at the beginning of the week. And then they continued to strengthen further. If we look at the long-term perspective - the whole of 2014, then the ruble exchange rate may sink against the dollar and the euro by at least 10%, our experts believe.

Our currency, it must be said, lost 10% of its value against the dollar and the euro in 2013. For one "American" in a year they began to give 3 rubles more, and for a "European" - 5 rubles.

Why is the ruble weakening?

The Russian economy is growing at a pace that is far from being as high as expected. “It used to be that the ruble fluctuated along with oil prices. They were key indicators that showed how much currency would come to our country from export proceeds,” explained Oleg Ivanov, Vice President of the Association of Regional Banks. Now the leading indicator for the exchange rate is the level of economic growth. The market is guided by this figure, but even if the cost of a barrel is more than $100, our economy is growing at a slow pace. In 2014, according to Ivanov's forecasts, our GDP will rise by 1.5%, below the global level. And this means that in 2014 the ruble will also suffer.

“But even sharp jumps in exchange rates are not at all critical for Russians,” Ivanov assures. The fact is that these fluctuations are an everyday thing. “If a person buys goods for the currency of his own country, then he does not need to monitor exchange rate changes,” the analyst says. This was relevant, say, in the 1990s, when a decent part of the price tags in stores was written in "conventional units." But a lot has changed since then. On the whole, the Russian foreign exchange market has strengthened.

It is impossible to say unequivocally that it is the weakening of the ruble that causes the rise in the price of imported goods on the shelves. First, no one canceled the usual inflation. Secondly, contracts for the supply of goods to Russia from abroad are not concluded every day. This means that the final prices for them do not directly depend on daily exchange rate indicators. Certain goods can rise in price, of course. But it is still too early to talk about a general trend towards a serious rise in prices for all imports.

Has the devaluation begun?

Still, in 2014 we definitely need a stable ruble. “If its rate starts to “play badly”, this can seriously affect the market and demand for domestic goods,” said Alexei Mamontov, president of the Moscow International Monetary Association. In his opinion, any downward movement of the ruble to help the Russian manufacturer is an illusion, it usually helps the economy only for a very short period, and the current weakening is beneficial only to speculators in the market.

Nevertheless, what is happening now with the ruble exchange rate happened all last year. And it is impossible to call it a devaluation, even if it is “soft”, Mamontov convinces: “It occurs only when there are serious fundamental grounds for it. Exchange rates alone are not enough to talk about it. Devaluation is always accompanied by a large level of public debt and a serious deterioration in the balance of payments. None of this is currently observed in the Russian economy.”

The exchange rate of the ruble against the dollar and the euro is determined by the ratio of supply and demand in the market. And now the Atlantic wind is definitely blowing: the US and the European Union are beginning to get out of the economic crisis of recent years. And this inevitably causes a great demand for their currencies, which, of course, has a negative impact on the rate of our money.

2014 is unlikely to be a year for risky investments and generally for experimenting with your own money. Traditionally reliable, in spite of everything, bank deposits remain. “True, it will hardly be possible to earn large interest on deposits, in general, only to save money from inflation,” says financial analyst Sergei Suverov. The reason is simple - bankers now prefer to reduce deposit rates.

But there are enough banks in Russia that will attract customers with high and even ultra-high interest rates on deposits. And now is the time to think: is the game worth the candle? “It is better to be wary of unreliable banks, and invest in relatively large ones,” Suverov is sure. Especially if more than 700 thousand rubles are stored on one deposit. If you plan to deposit an amount of less than 700 thousand into your account, which is fully compensated in the event of a bank failure, then you can take a risk and invest at high interest. But before doing this, you must make sure that the bank is included in the deposit insurance system.

Another question is what currency to keep your savings in? Expert advice on this matter is always the same: you need to put money into a bank account in the currency in which you are going to spend it later. But if you are determined to play for a long time and forget about an open account for a while, do not touch it, then, according to Suverov, the best type of deposit for 2014 is in foreign currency. “Moreover, in backbone, large banks, for a period of a year,” he clarifies. The yield expected by our expert on such a deposit in 2014 is at the level of 10%.

However, converting all your long-term savings into dollars and euros would not be the best solution. It is necessary to leave about 30% of your long-term contribution in rubles. This is how you can get rid of the risks of currency fluctuations. And they will still be, Suverov is sure.

In 2014, investment instruments that are more exotic for ordinary Russians should also be handled with caution. For example, last year turned out to be a failure for gold: a troy ounce fell in price by $400. And it's not a fact that gold will feel better. “Forecasts are still negative,” the analyst states. Now the ingot costs buyers $ 1,200. Expert "RG" advises to wait for the summer. According to him, if there is an increase in metal prices, then in the second half of the year, up to a maximum of $1,400 per ounce.

It is worth monitoring investments in securities and mutual funds (mutual funds) more closely. Over the past year, they have brought a yield of hardly more than 1%, which is very small for stocks. "On horseback", according to Suverov's forecasts, will be only selected sectors of the stock market - consumer, telecommunications and oil and gas.

Of course, those who like to keep money at home, “under the mattress”, will lose some of their savings in 2014 as well. The inflation rate, according to forecasts of the Ministry of Finance, will be in the range of 5-5.5%.

Here is another informative material for those who are interested in the safety of their hard-earned money. This time, as a preface to the article, I will give not my own comment, but a comment from the source site:

In the ruble, of course, it is more profitable to keep money than in foreign currency. Now. For some time. But in the next crisis, you will lose everything that you managed to earn, and given the constancy with which they happen (1998, 2008, 2014), is it worth the risk. So, if you are not a professional predictor, it will be more reliable in the currency. As for real estate. On the outskirts of Moscow, the cost of 3 rooms. apartments about 10 million rubles. It is really possible to rent it now (yet) for 35-37 thousand rubles. Minus the tax - it will turn out somewhere around 4% per annum. In rubles! As far as government incentives for mortgages are concerned, this is good. If you have a job and health. And the confidence that in the next 30 years you will still have them. And this, given the current state of the economy and health care, is not at all a fact.

After the collapse of the end of last year, the ruble began to grow. In April alone, the national currency strengthened against the dollar by 13%, and starting from February - by almost 25%. It is not surprising that now our compatriots are thinking about how to store their savings. Should they stay with the "wooden" ones in their hands, or should they still buy the "green" ones? Or maybe it's time to acquire real estate or stock up on gold bars? How to keep your hard-earned money in a crisis, found out "MK".

The Russian currency is strengthening. Inflation is also falling. According to Rosstat, over the past 8 months, its pace has slowed down, falling in annual terms by 0.5% to 16.4%. However, how long the ruble and inflation will please us is not precisely predicted even in the financial and economic bloc of the government. Too many factors can play both a plus and a minus for the domestic economy. In particular, these are oil prices, the geopolitical situation, as well as the current Western sanctions.

The reduction in real disposable income, which fell by 1.4% in the first three months of 2015, does not add optimism either. However, the population still managed to stock up on a certain amount of funds. So, for example, citizens, frightened by last year's autumn currency fever, converted some of the accumulated money into foreign currency. However, this year the ruble has taken revenge and is strengthening, and everyday needs are forcing our compatriots to return to the “wooden” ones.

But didn't the Russians hurry up by running to the exchangers? Maybe now it’s still worth holding on to the “green” or even buying real estate with these funds while they are?

As experience shows, when there is no money, we suffer from their absence. And when there are funds, our head is filled only with thoughts of where to invest them. And as profitable as possible.

Consider the main options for investing money.

Trust in the national currency

As practice shows, most citizens prefer to leave their money for safekeeping in banks. Thus, according to the Central Bank, in the first quarter of 2015, the total amount of deposits of individuals in Russian credit institutions increased by 2.9%, to 19.1 trillion rubles. Moreover, ruble deposits in March increased by 1.3%, while foreign currency deposits decreased by 3.3%. As experts explain, the reason for the growth is high interest rates on deposits. So, in November 2014, the average maximum rate did not exceed 7.7%, in December it rose to 12.4% due to the fact that the Central Bank immediately raised the key rate from 10.5% to 17%. At the moment, the average rate is 12.88%, despite the fact that the mega-regulator has reduced the key rate to 12.5% since May 5.

“Now it is best to keep savings in the national currency. And although the Bank of Russia has lowered the key rate, credit institutions offer quite attractive conditions for deposits, in particular for ruble deposits. In this case, it is better to give preference to banks with state participation. It is possible that in the autumn we will see the second wave of the crisis in small financial institutions, ”Sergey Gavrilov, chairman of the State Duma committee on property issues, comments on MK.

As for the currency, here experts advise to be more careful. The risk of losing your savings is high. “Investments in foreign currency in the current situation are inappropriate, since the dynamics of rates can change dramatically. As experience shows, private clients are more likely to receive a loss rather than income when using the currency as an instrument for investing funds,” Irina Grigorieva believes.

“It is risky to invest in a currency, because currency fluctuations are the most unpredictable. Dollars and euros can only be bought for current needs, for example, for holidays abroad,” recommends Anton Krasko, expert analyst at MFX Broker.

But if you still decide to convert your funds into currency, then give preference to "green". “If you choose between the dollar and the euro, then the advantage is with the American currency. The problems of the European economy will undoubtedly affect the euro exchange rate,” said Sergey Kozlovsky, head of the analytical department at Grand Capital.

However, if you are not ready to take risks by investing only in rubles or only in foreign currency, then it is best to use the “golden rule” and keep money in several monetary units at once.

However, do not forget that the deposit insurance system provides only 1.4 million rubles in compensation in the event of a bank failure. That is, if you managed to accumulate more than this amount, then it is better to “split” it into several deposits in different credit organizations.

Also, don't forget about inflation. And although in recent months it has been decreasing, according to independent experts, it could reach 18% by the end. In other words, it simply "gobbles up" interest on deposits.

Cashless entry to the stock market ordered

Unlike previous years, experts are betting on the Russian securities market. “The first half of this year is highly volatile against the backdrop of Ukrainian problems. However, we are already seeing the stabilization of the ruble exchange rate and oil prices. Therefore, the situation is expected to improve in the second half of the year, which will stimulate purchases on the stock market,” predicts Dmitry Shishov, head of the BCS Express department.

Moreover, according to Sergei Kozlovsky, certain assets have the potential to grow by 10% by the end of this year.

In order to start working in the stock market, you should acquire an investment portfolio. It includes a variety of securities, government and corporate bonds, treasury bills and certificates of deposit. The portfolio may also include gold, real estate and currencies. “You can choose assets for investment according to one of four criteria: by country, by industry, by the stability of dividends, or by the degree of diversification. So, for example, a portfolio of papers in the health sector ended last year in positive territory by 21%, while the portfolio of the utilities sector rose by 27%, and biotechnology - by 32%, ”explains“ MK ”the director of the analytical department of the IC“ Golden Hills -Kapital AM "Mikhail Krylov.

However, we must not forget that working in the stock market requires special knowledge, time and large sums of money. The latter must be at least $50 thousand. It is also extremely important to "choose the right time to enter and exit securities." Therefore, it is better to entrust the formation of a portfolio to professional management companies. “Your portfolio managers should be with more than 15 years of experience in the exchange and a double-digit return on assets under management. The methodology for determining the ratio of stocks, bonds and gold that the client needs is strictly individual. It all depends on the risk appetite. The main thing is that the portfolio manager is well versed in market movements and knows where to invest and how to choose the right combination of securities,” continues Krylov.

In any case, remember that the services of management companies are not cheap, and you will be able to receive a significant income from the investment portfolio only after a few years. In other words, if you want to make a quick buck, the stock market is not for you.

Investments worth their weight in gold

It seems that gold and silver are only of interest to the fairer sex. Investors currently prefer not to invest in precious metals, despite the opportunity to replenish their pockets. This is due to its specificity. “Against the backdrop of an unstable market, precious metals can show good returns. But it must be remembered that depersonalized metal accounts are not insured by the Deposit Insurance Agency. Therefore, this type of investment in a bank is very risky,” explains Irina Grigorieva.

You should also not hope to make real profits when working with physical metal. “Buying bars or coins is an inconvenient form of investment. When buying / selling ingots, a value-added tax of 18% is withheld, and coins can only be considered as an investment instrument “with a stretch,” the expert continues.

However, if you still decide to invest in the same gold, then be patient. “Investments in gold should be considered in the long term - more than 10 years. The current price on world markets in the region of $1,200 per troy ounce of the precious metal is favorable for acquisition, with the expectation that the value of the “yellow metal” will be $2,000 by 2023. We should no longer expect the same sharp increase in gold prices exponentially, which was observed until the end of 2013,” advises Pavel Shchipanov, head of the analytical department at Romanov Capital.

My home is my investment fortress

According to experts, the traditional investment tool during the crisis is real estate. True, if there are accumulated funds for that.

“Real estate is a tool that brings a stable income, but it also has a significant disadvantage - a high cost,” explains Grigoryeva.

However, you can use a mortgage loan. But again, you need a steady income. And the latter, as you know, has recently not only not been growing, but has been declining.

However, Sergei Gavrilov expects that by this autumn the real estate market will resume its growth. “Government measures to stimulate the mortgage of economy housing will allow it to be revived,” the deputy believes.

But now it's time to hurry up.

“During the period of growing delays in payment for supplied materials and bankruptcy of construction companies, the most rational thing is to buy new buildings at the final stage of construction and on the secondary market. Real estate objects in most regions of Russia (this situation can be seen especially clearly in Moscow and St. Petersburg) have lost more than 50% of their pre-crisis value since mid-2014, ”explains Pavel Shchipanov to MK.

At the same time, real estate, if necessary, can be rented out, especially in the capital. “On average, the rental yield brings up to 5-7%, depending on the type of property and area,” says Anton Krasko. “However, taking into account the annual price growth by an average of 10-15%, and the fact that the devaluation of the ruble cost per square meter also rises in price, the total return on such investments can reach 60-70% within 5 years.”

So the option of buying real estate and its further delivery is very good.

Let's summarize. It is possible and necessary to invest in Russia. However, in order for your money to “work”, you must responsibly approach the choice of an investment instrument. So, for example, a bank deposit can only cover inflation, and nothing more. However, there is a win-win option - it is to "invest in yourself and your children." In particular, it is worthwhile, if possible, to improve your skills, improve your health, or just go and relax. So, if you can only lose on one commission when converting currencies, and securities depreciate, your knowledge will always be in demand.

Irina Badmaeva

At the end of 2013, many banks reduced the rate on loans and slightly raised its size in deposit programs. This was especially noticeable in the autumn promotions, where the increase in interest was the most noticeable. Whether the same trend will continue in 2014 is a topical issue for many investors. But even more many are concerned about the choice of the deposit currency. Economic changes in the country and in the world make us think about the question in which currency is it more profitable to keep money.

It should be noted right away that not a single expert or analyst has a unanimous opinion on this matter, since the conditions for placing deposits in banks are regulated by the investment period, the conditions for using funds during the term of the deposit agreement, as well as the amount of investments and a number of other deposit parameters. Therefore, the choice of deposit currency largely depends on the tasks that the depositor sets for himself.

The main criteria for choosing a deposit currency

Usually, when choosing a bank and its conditions, depositors are guided by the size of the interest rate on the deposit - this indicator is most often decisive. However, in reality, it does not always have a significant impact on the profitability of the deposit, especially if the deposit is in foreign currency. One of the most important parameters for such deposits is the change in the exchange rate, which is observed during the entire period of the deposit.Throughout the past year, changes in quotations were observed for all foreign exchange assets, including the domestic ruble. Due to the slowdown in the domestic economy, the ruble had a chance to experience some pressure, which was reflected in its value in the financial market. As a result of this, we can expect a decrease in its quotes in 2014 against the euro and the dollar. Accordingly, banks will try to minimize risks by reducing interest rates on deposits and increasing them on the loan portfolio.

Unlike the national currency, the dollar is forecast to be in an uptrend, just like the euro quotes. Naturally, this situation will affect the purchasing power and the cost of goods. We should also expect an increase in import prices, which, again, will lead to a partial depreciation of the ruble and an increase in prices for consumer goods and products. Thus, the established interest rates on ruble deposits, even with their high rates, can only compensate for losses associated with rising prices and do not guarantee a special profitability.

Ruble deposits

As in all past years, the ruble has not yet become a stable currency and, as a means of investment, cannot guarantee the stability of the exchange rate. Ruble deposits have the highest interest rate, which today fluctuates in the range from 8.5% to 12%. Moreover, the upper limit is most often set at , which in themselves do not represent stability for investors.Despite such high rates in comparison with foreign currency deposits, the profitability of ruble deposits is declining due to inflationary processes that have been characteristic of the domestic economy for many years. The dynamics of the ruble exchange rate depends on the state of the economy in Europe and America, which are showing enviable stability. Thus, throughout the year we can expect, at best, the preservation of interest rates, but not their increase. Moreover, under unfavorable circumstances for the domestic currency, there is a risk of lower deposit rates in many banks on ruble deposits.

USD deposits

The stability of the American currency primarily depends on the state of the American economy and on the state of affairs in the global financial market. The stability of the dollar is largely due to the preferences of large investors around the world who keep their savings in this particular currency.

According to analysts' forecasts, in 2014 the upward trend in quotations for this currency will continue. Thus, deposits in dollars will continue to have a future. To date, the average rate for large banking institutions for deposits in dollars is 8-8.5%

, and in some regional banks this figure reaches 9-9.5%

per annum. Given the forecasted strengthening of the dollar against the ruble during 2014, it can be said with certainty that long-term deposits in dollars can be significantly more profitable than similar deposits in rubles.

Euro deposits

The level of interest rates on deposits in European currency is not much lower than dollar deposits. As of the beginning of 2014, the average deposit rate is 7.5-8.0% per annum. Over the past 2013, the euro showed a steady upward trend in the exchange rate. Moreover, such an increase was felt both in relation to the ruble and in relation to the dollar.

However, such circumstances do not give grounds to believe that the trend will continue in 2014. European countries do not benefit from the rapid increase in the value of their currency - the high price of the euro may adversely affect the recovery of the European economy. Accordingly, the artificial preservation of quotations at the level of the previous year makes foreign currency deposits in euros not as attractive to depositors as, for example, in dollars.

What to choose

As you can see, the profitability of deposits in different currencies is influenced by:- the value of interest rates;

- exchange rate changes.

Considering all the circumstances and adhering to the principles of risk diversification, the most successful placement of money in bank deposits will be opening a multi-currency account.

Short-term deposits, with a term of up to one year, can be opened in rubles. For longer periods, it is better to give preference to foreign currency deposits. Moreover, the greatest investment interest, taking into account all the above arguments, are dollar deposits.

Separately, it is worth paying attention to less popular currencies - Swiss francs and Japanese yens. The rates for exotic currencies are always higher and reach 12% per year.